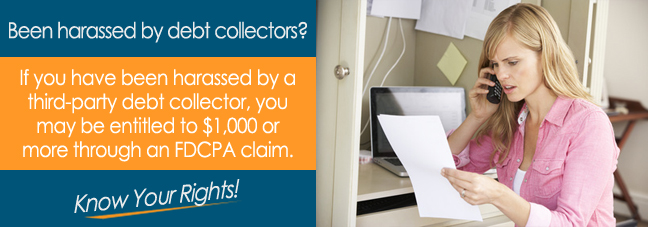

You have probably heard the expression, “Fool me once, shame on me; fool me twice, shame on you.” In the debt collection business, the shame for trying to fool you should be placed the first time when a debt collection agency tries to deceive you. In fact, you should turn deception into a legal case by invoking a federal consumer protection law.

Written into federal law by the United States Congress on September 20, 19777, the Fair Debt Collection Practices Act (FDCPA) forbids a long list of previously acceptable debt collection tactics. According to the FDCPA, a third party debt collector cannot threaten you in any way or call you at odd hours of the day.

The FDCPA also prohibits bill collectors from implementing deceptive debt collection tactics that include making false statements regarding consumer debts.

What False Statements Could NCM Management, Inc. Make?

A debt collection agency does not have to directly lie to you for it to be in violation of the FDCPA. The federal consumer protection law also protects consumers against the false statements made by a third party debt collector to another person or organization. You do not have to put up with a bill collector lying to a friend or a family member regarding your debt.

The FDCPA not only bans that type of deception, it also makes it illegal for a debt collection agency to contact a third party regarding any aspect of an outstanding credit card or personal loan account. A company in the debt collection business cannot make false statements about you to any of the three primary credit reporting bureaus.

False Statements Have to Be “Material”

For most provisions of the FDCPA, all an accomplished FDCPA attorney has to do is prove a third party debt collector committed one or more violations of the federal consumer protection law. For the false statements provision, recent court rulings have added an additional stipulation for proving false statement cases.

You must show the false statements issued by a bill collector had a “material” impact on how you reached personal financial decisions. Let’s say NCB Management, Inc. made a false statement regarding your debt. To win your case in a civil court, you have to show the false statement negatively affected the ability for you to evaluate all your financial options.

Seeking Monetary Damages in a Civil Court

After consulting with a licensed FDCPA attorney, he or she might recommend you file a lawsuit against the bill collector that violated the false statement provision of the FDCPA. The groundbreaking federal consumer protection law includes a provision that permits consumers to file claims seeking monetary damages.

Actual damages cover the costs associated with physical and/or emotional distress symptoms. Enduring the illegal tactics used by a debt collection agency can trigger emotional issues like mood swings and sudden outbursts.

![Did NCB Management, Inc. Make False Statements Regarding Your Debt?]()

Confer with an Experienced FDCPA Attorney

Filing a claim will prompt a third party debt collector to work with its team of highly skilled lawyers. You cannot afford to into a civil court alone against a high-powered legal team. Schedule a free initial consultation with a consumer protection lawyer who specializes in litigating FDCPA cases.

Additional Resources

*Disclaimer: The content of this article serves only to provide information and should not be construed as legal advice. If you file a claim against NCB Management, Inc., or any other third-party collection agency, you may not be entitled to compensation.